Real Returns – Less Emotion, More Reality

Recently, the Dutch Minister of Finance announced that the proposed legislation to tax actual investment returns in Box 3 is being reconsidered. As a result, the implementation of the proposal in its current form is no longer politically certain.

This reflects a broader reality: fiscal frameworks around private wealth remain fluid.

For many of our clients, Box 3 plays a limited or indirect role. Assets are often held within holding or family office structures. Yet the debate remains relevant — not because of the specific rule, but because it illustrates how quickly the rules of the game can shift, and how emotionally these shifts are often interpreted.

Concluding that investing “no longer makes sense” because of tax changes confuses policy changes with economic reality.

The question is therefore not only what changes fiscally.

The real question is how wealth owners continue to operate rationally under changing rules.

What Actually Changes?

Under the current Box 3 system, taxation is based on a deemed return of roughly 6%, regardless of the actual investment outcome.

In the proposed new system, actual returns would be taxed instead.

At first glance, this appears to be a fundamental shift. In practice, the difference is methodological rather than principled: returns were always taxed — the old system simply relied on assumptions rather than outcomes.

The proposed system also introduces something the old system lacks: loss carryforward. Investment losses can be offset against future gains.

This makes the tax framework path-dependent: the sequence of returns matters.

And that is precisely where nuance becomes necessary.

The Misconception: “You Are Always Worse Off”

Based on 12,000 simulated return paths (average return of 6% with 11% volatility — comparable to a balanced risk profile), a more nuanced picture emerges.

The results show:

- For smaller portfolios near the tax exemption threshold, the current system is often more favorable.

- For larger portfolios, this advantage gradually disappears.

- In poor return scenarios, the new system can actually be more favorable due to loss compensation.

- In exceptionally strong and uninterrupted positive return environments, the current system remains more advantageous.

In other words, the new system is not inherently worse.

It does not reward consistently positive return paths.

Instead, it offers protection against prolonged periods of poor returns.

From a purely economic perspective, that is a defensible structure.

The Real Issue: Inflation

The relevant question lies elsewhere.

Taxes are levied on nominal returns, while purchasing power is determined by real returns.

If an investment generates 6% annually while inflation is 3%, the effective increase in purchasing power is only 3% before taxes. After taxation, that number becomes significantly smaller.

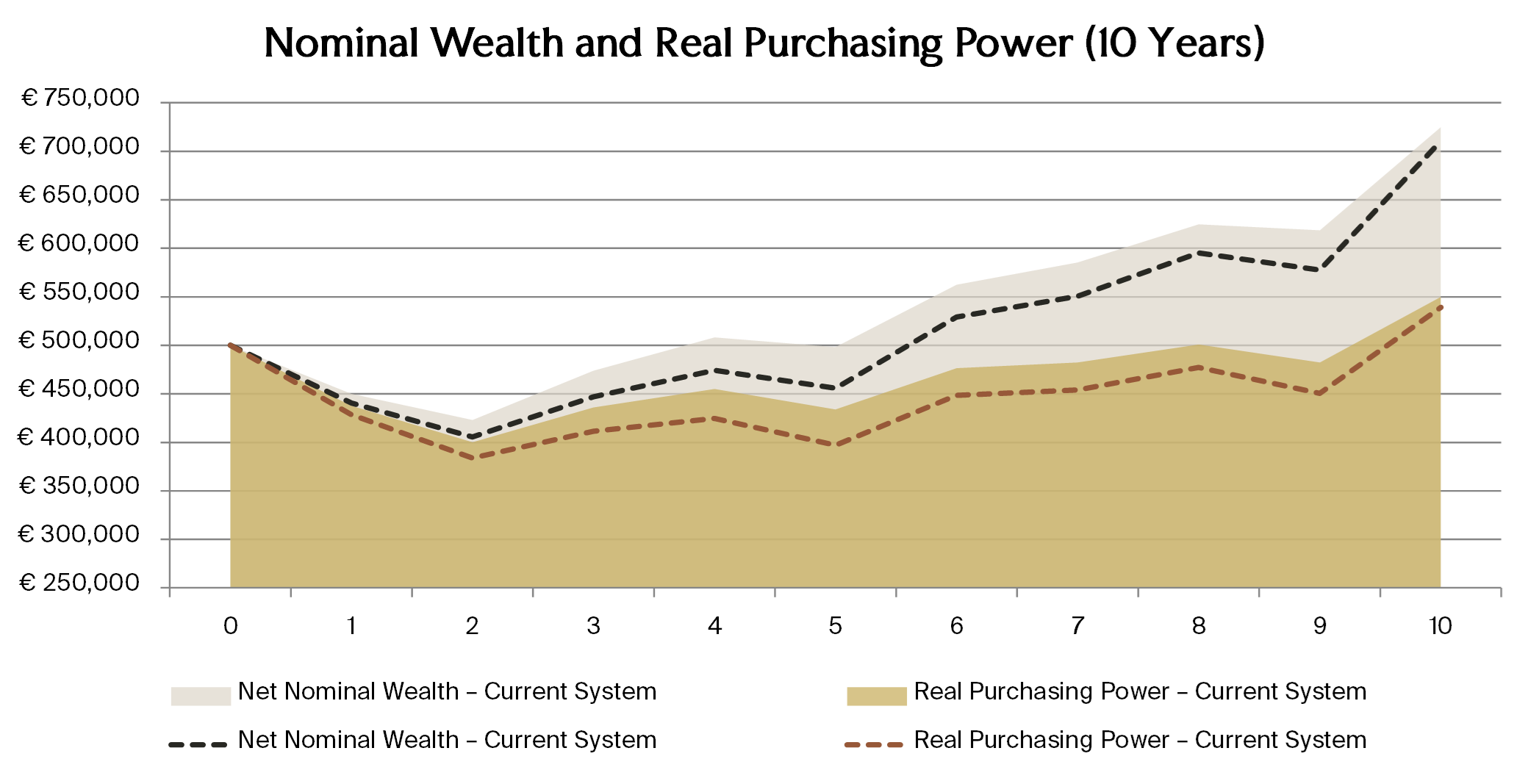

Figure 1: Nominal Wealth and Real Purchasing Power Under the Current and Proposed Box 3 Tax System, 10-Year Simulation

In many cases, inflation has a larger impact than taxation.

Anyone focusing only on nominal numbers misses the real story.

An illustration:

- €500,000 invested at an average return of 6% grows to roughly €710,640–€724,670 after 10 years (depending on the tax system).

- Adjusted for 2.8% inflation, this translates to roughly €539,160–€549,810 in purchasing power.

- By comparison, if the same €500,000 were kept in savings at an interest rate of 1.5%, it would grow to roughly €553,340–€557,040 (depending on the tax system). Adjusted for inflation, purchasing power would fall to roughly €419,820–€422,620.

In other words, the decision not to invest — often driven by frustration with taxation — can economically prove to be the most costly outcome.

In this example, inflation erodes purchasing power more than taxation.

Yet it often receives far less attention in the public debate.

What Does This Mean Strategically?

The proposed Box 3 framework:

- Makes the sequence of returns more relevant

- Increases the value of loss compensation

- Shifts the savings versus investing debate from fiscal to economic considerations

- Does nothing to change the structural role of inflation

The system is clearly under pressure. Questions about double taxation and the absence of inflation adjustments are legitimate.

But concluding that investing no longer makes sense is a mathematical misunderstanding.

In fact, in a world where inflation remains structurally present, rational investing becomes more important — not less.

Our Perspective

At RAMM, we do not react to fiscal noise.

We focus on managing risk across complete market cycles.

Taxes are a constraint.

Inflation is a constant.

What ultimately matters is how an investment strategy behaves under different scenarios.

Peace of mind does not arise from perfect rules.

Peace of mind arises when a portfolio continues to function rationally — even under imperfect rules.

Peace of mind, even when markets — or tax regimes — shift.