Stocks Are Celebrating. The Bond Market Is Not.

There are moments when equity markets project optimism while the underlying financial infrastructure tells a different story.

This is one of those moments.

The bond market underpins virtually every price of capital: mortgages, corporate lending, government financing, private credit, and equity valuations. In 2024, approximately $145 trillion of fixed-income securities were outstanding worldwide—larger than the global equity market and larger than the annual size of the global economy.

That makes the bond market more than an asset class. It is the foundation of the financial system.

That is precisely why the recent rise in long-term interest rates deserves attention. Not because every move in rates signals a crisis. But because higher rates, combined with elevated debt levels, reveal something that could be ignored for years: the price of trust.

Trust Is Being Repriced

Governments do not borrow at rates they choose themselves. They borrow at rates investors are willing to accept.

When inflation remains persistent, fiscal deficits stay structurally high, and major foreign buyers become less predictable, the negotiation changes. Investors demand greater compensation for duration, inflation, and uncertainty. Technically, this is reflected in a higher term premium: the additional compensation investors require for lending capital over longer periods.

We can already see this in practice. Japan and China remain among the largest foreign holders of U.S. Treasuries, but their paths have diverged. China has steadily reduced its position over recent years, while Japan remains the largest foreign holder at approximately $1.19 trillion.

The key point is not that foreign buyers are abandoning U.S. debt. It is that the automatic absorption of U.S. government debt has become less straightforward.

This is not evidence of panic. It is evidence of structural change.

The world that absorbed U.S. debt for decades with little debate has become less predictable.

The Central Bank Is Caught in the Middle

Under normal circumstances, central banks can respond to economic weakness by lowering interest rates—monetary easing—to support credit creation, consumption, and asset valuations.

But that response only works as long as markets believe inflation will remain under control over the long run.

If investors begin to suspect that rate cuts will reignite inflation, the bond market may demand higher yields instead. Federal Reserve Governor Christopher Waller recently suggested that he is no longer inclined to favor rate cuts. In his view, rate cuts are no longer more likely than rate hikes.

He described rate increases—monetary tightening—as premature in the near term. But over the longer term, he did not rule them out if investors and consumers lose confidence that inflation will return to the central bank’s target.

That is the essence of the problem.

If central banks ease policy too quickly, the bond market may interpret that as an inflation risk. Short-term rates may fall, while long-term rates rise anyway.

If central banks remain too restrictive, pressure builds across the economy, real estate markets, credit markets, and government finances.

This is not a traditional recession concern.

It is a question of trust.

Why Stocks Continue to Rise

Equity markets can remain optimistic for a long time, even when the bond market is sending warning signals.

That is not irrational.

Stocks often price in future liquidity: the expectation that policymakers will ultimately step in to provide support.

But that also makes the starting point more fragile.

When equities are richly valued while bonds simultaneously demand higher real compensation, an uncomfortable tension emerges. The risk-free rate is no longer a theoretical concept. It becomes a genuine competitor for capital.

For affluent investors, the question is therefore not:

Will there be a crisis?

A better question is:

How much of my portfolio depends on a single outcome?

The Problem with Forecasting

Many investment portfolios are implicitly built on stability: declining interest rates, accommodative monetary policy, expanding profit margins, and central banks willing to intervene when markets fall too far.

But in an environment where inflation, interest rates, and geopolitics reinforce one another, forecasting becomes more dangerous.

Not because analysis is worthless, but because the range of possible outcomes becomes wider.

That is why it is no longer enough to have a view on interest rates, gold, equities, or currencies.

The question is not whether your portfolio reacts.

It always does.

The real question is whether your portfolio contains components that can consciously adjust risk when market regimes change.

Where RAMM Becomes Relevant

RAMM was not designed to predict when the bond market will break, when equities will reverse, or when central banks will change course.

RAMM was designed to follow market dynamics when market convictions begin to shift.

That distinction matters.

The model does not reduce risk based on headlines, expectations, or isolated events. It adjusts risk based on price behavior, trend quality, and changing market structure.

When markets repeatedly reverse direction before a trend can establish itself, the environment is challenging. But when a genuine regime shift occurs, it becomes essential to respond systematically rather than emotionally.

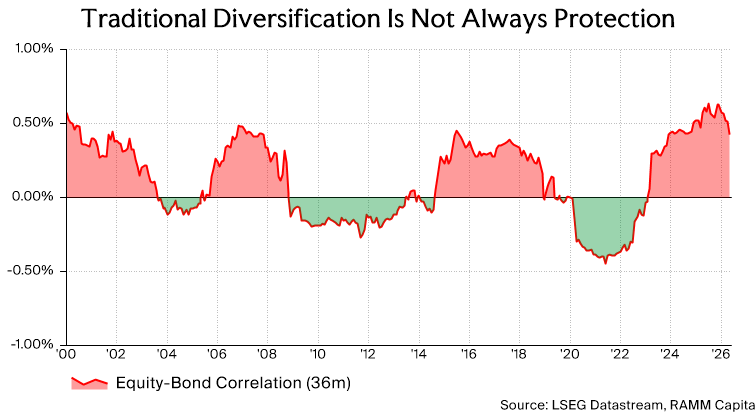

In a world where bonds no longer automatically provide protection and equities are no longer automatically rewarded, adaptability becomes more valuable.

Not as a replacement for a broader wealth structure.

But as a component that does not depend on the same assumptions as traditional portfolios.

RAMM Is Not Passive

For RAMM, peace of mind is not the same as doing nothing.

Peace of mind means decisions have been considered in advance. It means risk is adjusted according to market dynamics. It means there is no need to form a new opinion every time interest rates move, geopolitical tensions escalate, or inflation data is released.

The bond market is showing us that trust is being repriced.

At times like these, there is value in a strategy that does not need to know how the story ends, but is designed to adapt when the story changes.

That is not a promise of protection from every shock.

It is an approach to investing that does not require being right about the future. It requires being prepared for change.

And in a world where markets are becoming less predictable, that is precisely what serious capital increasingly needs.

1 For comparison, the global equity market was valued at approximately $115 trillion in 2024, while global gross domestic product (GDP) amounted to roughly $110 trillion.