Looking back to 2024, looking forward into 2025

Intro

This is the fourth annual review since the start of RAMM Global Assets in 2021. Not our own preview this time. However, an overview of what seven influential institutions expect for 2025, so that a picture of the consensus is created. And where the market is vulnerable if that consensus does not come to fruition.

Consensus is rarely a good guide for investments. Because what everyone expects is usually already included in the price. We therefore do not use consensus as a prediction. But as a mirror for what can go wrong. And what that means for the markets.

Looking back at markets

US stocks once again strongly outperformed most other markets in 2024. The 'Magnificent 7' pulled the bandwagon again. But the wider US market also performed well including mid- and small-caps. Investors clearly preferred the US market. Outside the US, sentiment lagged behind. Especially after Trump's election, when higher trade tariffs were priced in.

The US economy remained remarkably resilient in 2024 as well. Europe the picture was less rosy. Due to a lack of decisiveness, declining competitiveness and high energy prices. China failed to stimulate domestic demand. High debt and low consumer confidence weighed on growth. This weighted on emerging markets.

The increase in gold was also remarkable. +35% in euros, despite headwinds from a strong dollar and higher interest rates. The demand seems seems to have a firm basis. Central banks buy gold as a reserve. Investors as a safe haven.

The US-dollar profited from the US economic growth. After Trump's election, an extra boost followed. Especially because of his plans for higher import tariffs and tighter budgetary discipline.

Bonds and real estate had a moderate year. Nevertheless, in euros, they delivered decent returns thanks to the strong US-dollar.

High-quality bonds benefited from stable inflation and loose monetary policy. High-yield debt was supported by investors' appetite for risk. Indirect real estate lagged behind. Higher mortgage rates and construction costs weighed on returns.

Review of RAMM Global Assets

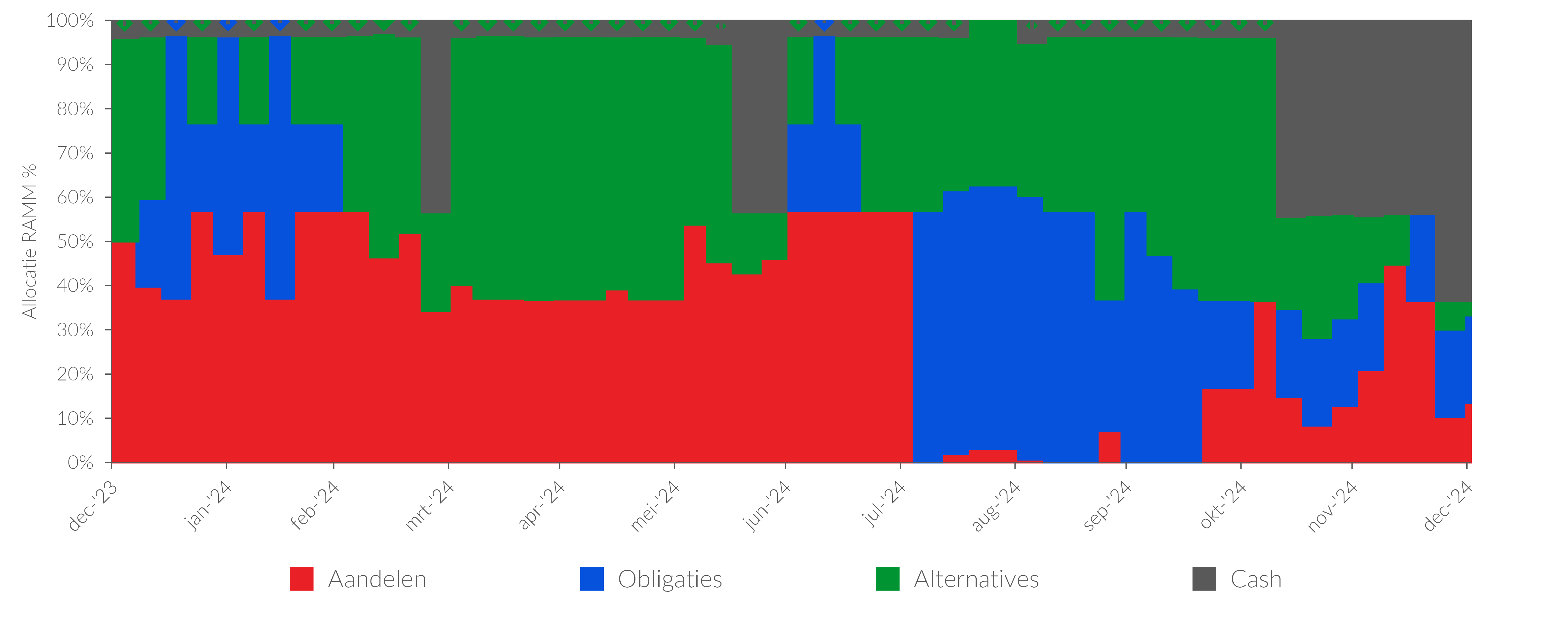

Figure 1: RAMM Global Assets Fund Allocations, 2024

RAMM had a bias towards stocks and gold in 2024. Stocks weighed 34.6% on average, with a clear preference for the US. Gold was its dominant position within alternatives. Both choices contributed substantially to the fund result: gold +6.2%, US stocks +4.9%, both in euros.

The low correlation between the positions ensured a stable development of the fund through the year. From November, the US dollar also had a strong place in the portfolio. The average cash position in 2024 was 9%. The allocation followed the system. The result was rest.

Figure 2: RAMM Global Assets Fund Attribution, 2024

2025, consensus and risks

For 2025, we base ourselves on the outlook of seven influential parties, including BlackRock, JPMorgan, and Vanguard. What is striking: they are unanimously positive about US risky investments. And they are remarkably confident in their own scenario.

That confidence is remarkable. Especially considering the expected policy changes under Trump. The consequences are potentially huge, complex and difficult to predict. Nevertheless, the red line is clear: people believe in the resilience of the US economy. And in the positive effect of Trump's measures.

The consensus is therefore strong and positive about American equities. This makes the market vulnerable. Because what is widely expected is usually already discounted. And the stronger the conviction, the greater the shock if the outcome is different.

The table shows what can then happen to the markets if the consensus expectation does not come true.

According to the consensus, the US economy will remain the strongest in 2025. Expected growth: 2.5%. AI is seen as the driver. Higher productivity leads to profit growth. BlackRock even speaks of “mega forces” that break historical trends.

This explains the high valuations in the US. And, according to all parties, the US remains 'the place to be' for stock investors.

For Europe, the opposite is true. Expectations are low. Due to stagnant growth, weak policies and high costs. Import tariffs from the US also play a role. Despite their lower valuations, European stocks remain unattractive, according to the consensus.

The mood is also cautious for emerging markets. China, in particular, remains vulnerable. High debt, low consumer confidence and US import tariffs are weighing on growth. Other emerging markets are feeling this through lower commodity exports and higher import costs, partly due to the strong dollar.

The dollar will remain strong, according to consensus. That would be a headwind for many countries outside the US.

Both the FED and the ECB are expected to lower interest rates further. Inflation allows that for now. But the risks are at the higher end. Especially in the US. Nevertheless, under Trump, pressure would increase on the FED to cut earlier and more. Expectation: two to four rate cuts in 2025.

Inflation remains the determining factor for bonds. Expectations are moderate. That is why people are neutral on bonds. But the risks are on the downside.

According to consensus, gold remains in demand. Central banks continue to buy. Investors continue to seek protection against geopolitical risks.

People are less positive about raw materials. Demand for oil and metals appears to be weakening.

Risks

The biggest risk for the baseline scenario is an unexpected increase in inflation in the US. That would affect bonds. But also stocks, real estate and high-yield debt. Growth stocks, which are now supporting sentiment, are particularly vulnerable. Their risk premium is low. The rest of the world is less sensitive, due to weaker growth. But high-quality bonds will also suffer from rising interest rates if inflation rises.

There are several reasons why inflation can rise in the US. Higher import prices, trade tensions, less supply of cheap labour and overheating of the economy. According to the consensus, the chance of this is rather small. But the impact of a surprise could be huge. Especially on US growth stocks.

Geopolitics also remain a source of uncertainty. The fall of Assad in Syria reduces the risk of escalation in the Middle East. And Trump appears to be open to talks with Russia. At the same time, his unconventional style increases unpredictability. His proposals about Greenland and Panama show a different view of the world order. Less focused on stability. More on power.

Whether that works out well or badly for markets is impossible to say with much conviction. But there is less predictability than before. That is exactly what requires vigilance. Not on the basis of fear. But as a matter of principle. Because calm doesn't come from what you know. But from what you factor in.